Understanding Your Payslip

Whether it’s your first payslip or if you’ve been working for years, it’s still important to know how your pay is worked out. Your payslip contains important information, including your payroll number, your gross and net pay, and normally your tax code. It’s important to understand your payslip and how to make sure you’re being paid the right amount.

Your right to a payslip

All employees and workers are entitled to an individual, detailed written payslip – when, or before, they’re paid. Your written payslip doesn’t have to be on paper – it can be sent to you by email or accessed through a website.

The right to a payslip applies to casual staff as well as employees. It doesn’t apply to independent contractors or people working freelance.

Understanding your payslip

1. Your personal information - Your name, and sometimes your home address, will be shown.

2. Your payroll number - Some companies use payroll numbers to identify individuals on the payroll.

3. Date - The date your pay should be credited to your bank account is usually shown.

4. Tax period - The number here represents the tax period for that payslip. For example, if you’re paid monthly, 01 = April and 12 = March.

5. Your tax code - Your tax code will be sent to you by HM Revenue & Customs (HMRC).

The code tells your employer how much tax-free pay you should get before deducting tax from the rest. If the code is wrong, you could end up paying too much or too little tax. So it’s important to check this against your latest tax code notice.

There’s more about tax codes, and why it’s important to check them, later in this guide.

6. Your National Insurance number - You must have a National Insurance number to work in the UK. You have the same NI number throughout your life – even if you change your name.

It’s your personal number for the entire social security system. It’s used to make sure all your contributions are recorded properly, and helps to build up your entitlement to state benefits – such as a pension.

7. Payments, wages, bonuses and commission - This will show how much you’ve earned in wages before any deductions are made. It might also show how your pay was calculated. For example, your hourly rate and the number of hours worked.

It could also show any extra payments you’ve earned on top of your basic pay, such as like bonuses, commission or overtime.

8. Expenses - Your employer might pay any expenses owed to you via the payroll.

Some employers will list each expense payment separately on the payslip. Others combine them to show a taxable or non-taxable amount.

9. Deductions – tax and National Insurance - Your payslip must show the amount of variable deductions, such as tax and National Insurance

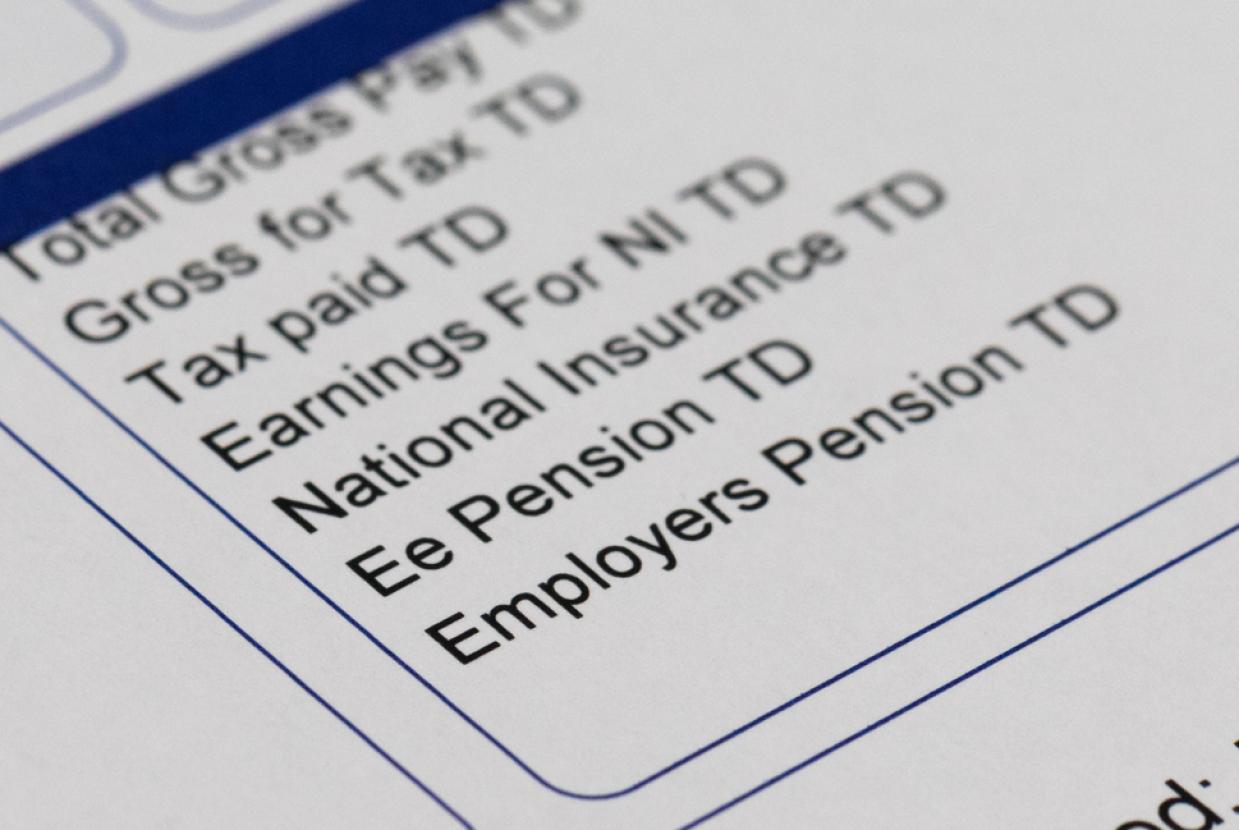

10. Pensions - If you’re paying towards a workplace pension that your company has set up or arranged access to, the amount you’re contributing will be shown.

If your employer is contributing too, that amount might also be shown.

A court can order deductions directly from your pay. For example, for unpaid fines or for debt repayments to be handed to your creditors.

The Child Maintenance Service (CMS) can also ask for a Deduction from Earnings Order for the maintenance of a child.

If these orders are made for deductions, the employer can, if they choose, take an extra £1 as an administration fee.

This fee can only be charged if a deduction or partial deduction has been made. Employers often waive the fee. But if they deduct it, it must be shown separately on the payslip with a description.

13. Sick pay - What’s shown on your payslip will depend on how long you’ve been ill and your company’s sick pay policy.

Your employer is liable to pay you Statutory Sick Pay if you’re off work sick for four days or more in a row, and you meet certain conditions.

Statutory Sick Pay is treated like the wages or salary it replaces. So your employer will make deductions for things like tax, National Insurance and student loans.

Under your contract, you might also be entitled to occupational sick pay. This will usually be shown as a separate figure – any Statutory Sick Pay is likely to be deducted from occupational sick pay.

14. Maternity, paternity and adoption pay - Are you a mother who isn’t at work because you’ve just had a baby and you’re getting Statutory Maternity Pay? Then this will be shown on your payslip.

You might also receive maternity pay, which will usually be shown separately. If parents choose to share time off, and take Shared Parental Leave, they might be paid Shared Parental Pay.

If a child is adopted, Statutory Adoption Pay will be paid to the new parent staying at home for a period after the adoption. If a couple jointly adopts, the other partner can be eligible for Additional Statutory Paternity Pay.

Again, you must meet certain conditions to be able to qualify for these payments. They’re all treated in the same way as ordinary earnings for tax and National Insurance.

15. Workplace benefits - Do you get health insurance through your workplace or have a company car? Then these will be listed on your payslip and can affect your tax code.

It might also show repayment of season-ticket loans, cycle-to-work scheme loans and charitable donations (using the give-as-you-earn scheme). If you’ve signed up for one of these, it should show up on your payslip

16. Other deductions - Any other deductions, such as trade union subscriptions, should be shown.

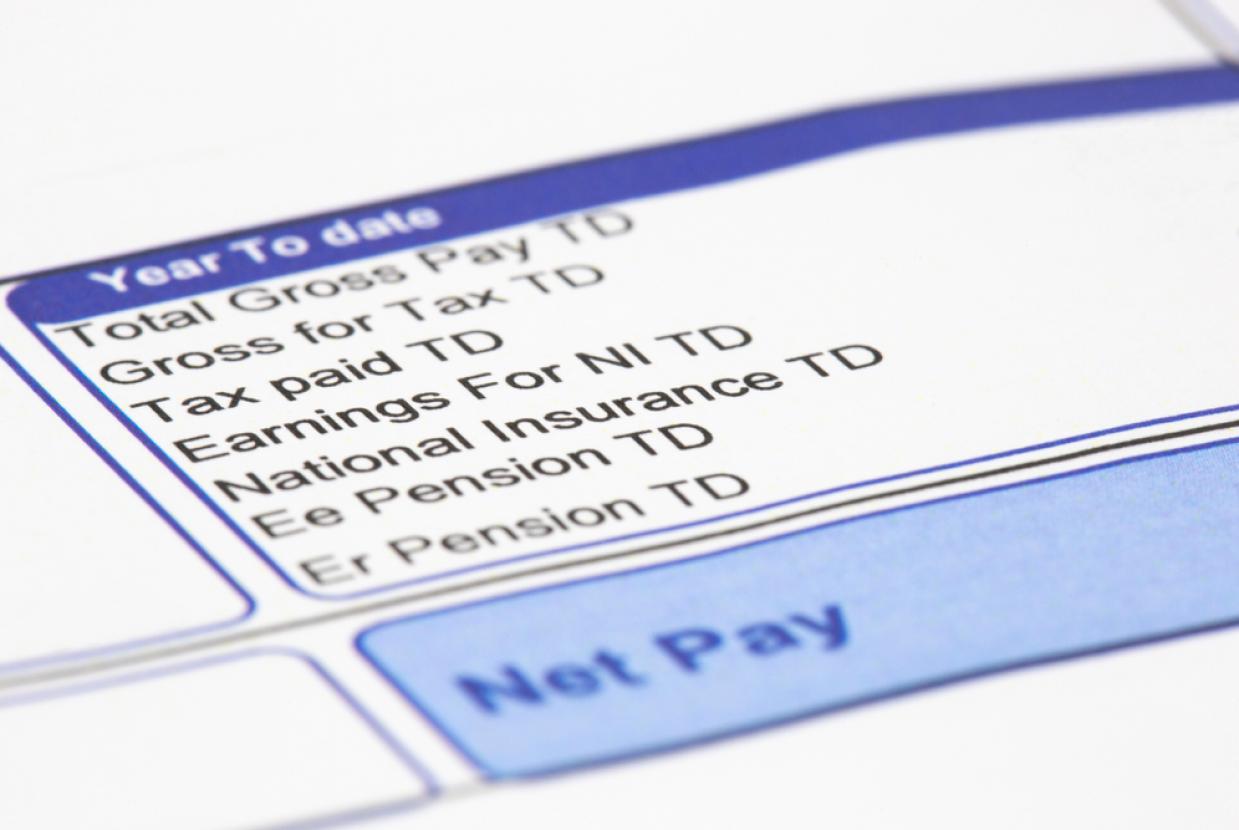

17. Summary of the year to date - Your payslip might show how much you have been paid so far in this financial year. A financial year runs from 6 April to 5 April.

It might also show totals for how much you’ve paid in tax, National Insurance, student loans and pensions.

18. Net pay – what’s left - For many people, the most important figure on their payslip is net pay.

So, what is net pay? It’s the amount you get when all the deductions have been made. It’s a good idea to check this against your bank statement to make sure it matches what’s paid in.

19. Important messages - Some employers use a space on the payslip for important messages. These might give you extra information about your pay or other information they want to share.

What is a tax code?

The amount of tax you pay depends on:

- how much income you have

- how much tax you’ve already paid in the year

- your Personal Allowance.

Different people have different tax codes, depending on their circumstances. Every year, HMRC sends out a Coding Notice. This tells you what your tax code is and how much tax you’ve paid.

You can also find your tax code on your payslip. It’s usually made up of a few numbers and a letter.

How is my tax code worked out?

Your tax code is normally the amount you can earn without paying tax, divided by 10, with a letter added.

For example:

- Tax code: 1257L

- 1257 becomes £12,570 earned before tax.

My tax code starts with BR

- This means you’re not getting your tax-free basic personal allowance – so all your income is being taxed at the basic rate of 20%.

- This can happen if your employer doesn’t have all the information they need to work out your tax code.

It doesn’t always mean you’re paying the wrong amount of tax. For example, you might have two jobs and HRMC have allocated your personal allowance against one of these.

My tax code has no number, or starts with D followed by a number. This is usually because you have more than one source of income.

Your Personal Allowance is used up on your main income source, and you pay tax on everything you earn from your second income source.

For example, you might work a main job during the day and do shifts in a pub or work in a factory in the evenings.

If you earn more than £12,570 a year (for 2021-22) in your main job, your second job will be taxed at the basic rate. This can also apply to pensions or money paid out by investments (dividends).

My tax code starts with K

This means you have tax from the past you still need to pay, or you get money or benefits that can’t be taxed before you receive it. For example, a State Pension or company car.

From this, your employer can work out how much should be paid towards what you owe.

The amount you pay will never be more than half the amount you’ve earned or received during the pay period. Regardless of whether that’s monthly, weekly or another period.

What is an emergency tax code?

Sometimes your tax code isn’t right for your circumstances and you might be given an emergency code.

An emergency tax code assumes that you’re only entitled to the basic personal allowance. It’ll mean you’ll pay tax on all your income above the basic personal allowance (£12,570 for 2021-22).

It won’t take into account any allowances or reductions and reliefs you might be entitled to. This could mean you pay more tax than you should be a short period of time.

For 2021/22, the emergency tax codes are:

- 1257L W1

- 1257L M1

- 1257L X.

You might be put on an emergency tax code if:

- you’ve started a new job

- you’ve started working for an employer after being self-employed, or

- you’re getting company benefits or the State Pension.

If your tax code is one of these, HMRC will automatically update it. But it might mean that for one or two months your pay won’t be the same, so be careful with your budgeting.

How do I check my tax code?

To make sure you’re on the right tax code, check your code matches the Personal Allowance you should be getting

What do I do if I think my tax code is wrong?

If you think your tax code is wrong, or if you’re in any doubt, contact HMRC. It’s important you give them all the information they ask for so you don’t end up on the wrong tax code and pay too much or too little tax.

Keeping your payslip

It’s important to keep your payslips in a safe place. Here are our top three reasons why:

- Security. Payslips contain a lot of personal information about you and your earnings, including your National Insurance number. Keep them safe to help avoid them being used for identity fraud.

- Recordkeeping. It’s a good idea to keep a record of all your earnings and tax payments in case there’s a problem and you need to check old details.

- Evidence of earnings. For some financial products, such as loans, you might be asked to prove your earnings by showing your last three payslips.

Different pay rates

Does your pay vary, depending on how long or when you work? Then your employer will have to include details of the hours you worked as well as how much you’ve earned on your payslip.

If you earn different amounts for different types of work, separate figures for both will have to be included on your payslip.

This change to legislation is aimed at employees who work variable hours and whose pay changes accordingly. This will make it clearer if you’re being paid at least the National Minimum Wage. Zero-hours contract workers will particularly benefit from this new legislation.

Content supplied by...